Introduction

Law school trains lawyers to argue cases, negotiate deals, and protect clients' assets. It does almost nothing to prepare them for managing their own finances.

That gap has real consequences. According to the ABA's 2024 student debt survey, 68% of young-lawyer borrowers reported that carrying student loan debt caused stress and anxiety — a figure that held at 67% even among respondents without debt.

Financial pressure doesn't stay in the background of a legal career. It shapes decisions about firms, practice areas, whether to make partner, and whether to stay in law at all.

This guide covers the financial concepts every lawyer needs to understand, how to build a personal financial strategy suited to an attorney's income, and why financial clarity is the foundation for any major career decision — including whether the next right move is inside the law or beyond it.

Key Takeaways

- Financial literacy for lawyers covers personal wealth management, debt strategy, and long-term planning, not just the economics of running a firm

- Core concepts like net worth, cash flow, tax efficiency, and retirement basics directly affect career sustainability

- Law-specific pressures (heavy debt loads, variable income, delayed compensation) call for strategies built around how attorneys actually earn and spend

- Know your financial baseline before any major career move, especially a transition out of practice

Why Financial Literacy Matters More Than Ever for Lawyers

The profession has started to acknowledge this gap. A few programs now exist:

The profession has started to acknowledge this gap. A few programs now exist:

- NYU Law offers Financial Concepts for Lawyers, a 10-hour course for first-year students covering accounting, business entities, finance, and statistics

- ABA Young Lawyers Division runs financial literacy programming, including Retirement Planning 101 for Lawyers and a 2026 resource on navigating the federal loan landscape

- AccessLex's MAX program provides free personal finance coaching at 190 law schools

These are meaningful steps. But they remain optional for most JDs — not graduation requirements. That gap matters, because lawyers are entering the workforce carrying significant debt with no required training in how to manage it.

The Debt Reality

The numbers are significant. The ABA's 2024 debt survey puts average law school debt at graduation at $165,000. For Black and African American law students, LSAC's 2024 data projects average debt closer to $108,000, with 31% anticipating owing $150,000 or more.

None of that debt comes with instructions. Most new associates begin repaying loans while simultaneously building an emergency fund, starting retirement contributions, and navigating their first complex compensation structure — all without formal preparation for any of it.

The Mental Health Connection

Financial stress compounds an already demanding profession. A study of 12,825 licensed attorneys found 28% reported depression symptoms and 23% reported significant stress. Financial pressure isn't the only factor, but it's a consistent one. Thomson Reuters' 2022 Stay-Go Report found some firms faced associate turnover exceeding 125% over five years — a figure that points to financial stress and burnout, not just career dissatisfaction.

Core Financial Concepts Every Lawyer Must Understand

Net Worth and Cash Flow

These two metrics serve different purposes and both matter:

- Net worth = total assets minus total liabilities. It's your financial health snapshot, best calculated annually

- Cash flow = monthly income minus monthly expenses. It determines day-to-day stability and your ability to save, invest, or absorb unexpected costs

A lawyer earning a high salary can still find themselves cash-poor without disciplined spending habits. Net worth tells you where you are; cash flow tells you whether you're moving forward.

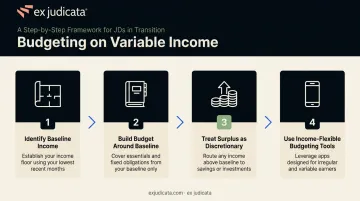

Budgeting for Variable Income

Many lawyers—especially those in litigation, contingency work, or on partnership tracks—don't earn the same amount every year. Budgeting to peak income is one of the most common financial mistakes in this profession.

A more stable approach:

- Identify a baseline income figure—the floor you can reasonably count on

- Build your budget around that baseline

- Treat income above the baseline as discretionary (savings, debt paydown, investment)

- Use budgeting software that accommodates irregular income patterns

Tax Efficiency and Business Structure

Tax planning is where legal professionals often leave the most money on the table. Key considerations:

- Self-employment tax is 15.3% for solo practitioners—a meaningful cost that salaried associates don't pay directly

- Business structure matters: A single-member LLC is treated as a disregarded entity by default, while an S-Corp election can allow a partner or solo attorney to split income between salary and distributions, potentially reducing self-employment tax exposure

- Deductible expenses for solo practitioners include malpractice insurance, home office costs, and CLE—but only if properly documented and legitimately business-related

- Equity partners shift from W-2 income to K-1 partnership income, meaning they owe tax on their distributive share whether or not it's distributed, and must make quarterly estimated tax payments

Choosing the wrong structure early is worth fixing. Many solo practitioners find that switching to an S-Corp election above $80,000–$100,000 in net profit meaningfully reduces their annual tax burden—consult a CPA familiar with law firm structures before filing season.

Debt Management and Law School Loans

Repayment strategy is one of the highest-stakes financial decisions a lawyer makes, and it's typically locked in during the first year out of school. As of 2026—following the court invalidation of the SAVE plan—the available income-driven options are Income-Based Repayment (IBR), Income-Contingent Repayment (ICR), and Pay As You Earn (PAYE).

Key decisions to get right:

- PSLF eligibility: Government and 501(c)(3) nonprofit lawyers who work full-time and make 120 qualifying payments can pursue Public Service Loan Forgiveness—but only on Direct Loans

- Private refinancing trade-offs: Refinancing federal loans into private loans eliminates IDR access and PSLF eligibility permanently. The CFPB explicitly warns against this move for borrowers who may need federal protections

- Choosing wrong early costs real money: Mismatched repayment plans—particularly for high earners who'd be better served by aggressive paydown—can result in unnecessary interest over a 10-20 year horizon

Investment and Retirement Basics

Deferring retirement contributions until debt is paid down is one of the most expensive decisions a lawyer can make quietly. A $10,000 contribution at age 28 grows to roughly $75,000 by age 65 at a 5% average annual return—that same contribution made at 38 yields less than half that amount. Starting early matters more than starting large.

Current 2026 IRS contribution limits:

| Account Type | Annual Limit | Catch-Up (50+) |

|---|---|---|

| 401(k) / 403(b) | $24,500 | $8,000 |

| Traditional / Roth IRA | $7,500 | $1,100 |

| SEP-IRA | $72,000 | — |

Solo practitioners and small-firm lawyers should look closely at SEP-IRAs—the contribution ceiling is high, and contributions go in pre-tax. Associates at large firms often have 401(k) access with employer matching, which is effectively free money left behind when contributions are skipped.

Managing Your Personal Finances as an Attorney

Assess Your Financial Baseline First

No financial strategy works without an honest starting point. Your baseline should cover:

- All income streams (salary, bonus, distributions, side income)

- Total outstanding liabilities (student loans, mortgage, credit, other debt)

- Monthly fixed and variable expenses

- Existing savings, investment balances, and retirement accounts

- Insurance coverage gaps

Many lawyers underestimate their total debt or overestimate their savings, particularly when accounts are spread across multiple institutions. A formal annual financial audit—one document, all accounts—gives you a real net worth number and eliminates the guesswork.

Build a Plan Aligned to Your Career Stage

Financial priorities change at each career stage:

Early career:

- Establish an emergency fund (3-6 months of expenses)

- Select the right loan repayment strategy before it defaults into a suboptimal plan

- Begin retirement contributions even while in repayment

Mid-career:

- Shift focus toward wealth accumulation and tax optimization

- Evaluate risk management (disability insurance, umbrella coverage)

- Assess whether current business structure is optimized

Partner/senior level:

- Equity buy-ins require careful planning—capital contributions typically run 25-35% of compensation, with some Am Law 100 firms requiring up to 55% of a new equity partner's annual compensation

- The shift from W-2 to K-1 income changes cash flow patterns and tax obligations in ways that catch many new partners off guard

- Estate planning, succession planning, and maximizing tax-advantaged accounts become priorities

Protect What You Build

Building wealth is only half the equation. Protecting it requires the same deliberate attention — and for attorneys, the gaps in coverage can be costly:

- Disability insurance: A lawyer's income depends entirely on their ability to work. Own-occupation disability policies—which pay out if you can't perform your specific work, not just any work—provide meaningfully stronger protection than generic policies

- Professional liability (malpractice): Often required, but coverage limits matter

- Life insurance and umbrella coverage: Gaps here can erase years of wealth building in a single event

Financial Literacy as a Foundation for Career Decisions

Financial clarity isn't only relevant inside a legal career. It's a prerequisite for making any major career decision well.

A lawyer who doesn't know their net worth, monthly burn rate, or total debt obligations cannot accurately assess what it would take to negotiate a raise, launch their own practice, or change careers entirely. The math simply isn't available to them.

Calculate Your Financial Runway

Financial runway is the number of months you could sustain your current lifestyle without your current income, based on liquid savings and realistic expense reduction. Even a 6-month runway changes what's possible. A 12-month runway opens up considerably more options.

Building runway doesn't require dramatic sacrifice. It requires treating savings as non-negotiable before discretionary spending begins—the same discipline applied to baseline budgeting.

The Fear of Income Disruption

The most common barrier lawyers cite when considering a transition out of practice is financial uncertainty—specifically, fear of income disruption. Ex Judicata's Money Management content hub, which offers free editorial resources on compensation trade-offs, savings runway planning, and debt management through transition, puts it plainly: "the single most under-discussed obstacle to leaving law is the comp delta."

That fear is real. A Big Law associate or non-equity partner moving into a business role may face a 20–60% near-term pay cut. The number needs context, though:

- Many transitioning lawyers find compensation catches up—or exceeds prior earnings—within 3-7 years

- The fear is often tied to a lack of concrete financial planning, not an actual financial inability to make a move

- A lawyer who has calculated their runway, mapped their expenses, and understands their debt obligations can evaluate a transition on real numbers rather than anxiety

For lawyers weighing what comes next, financial planning and career exploration aren't separate exercises. Working through both at the same time makes the decision more concrete—and far less driven by anxiety.

How to Improve Your Financial Literacy as a Lawyer

Education and self-study:

- Seek resources tailored to legal professionals, not generic personal finance content

- The ABA Young Lawyers Division offers targeted programming on retirement planning and loan repayment

- AccessLex MAX provides free personal finance coaching at 190 law schools

- Ex Judicata's Financial Fluency for Lawyers ($195, taught by Notre Dame Professor Emeritus Matthew J. Barrett) covers financial statements, GAAP, time value of money, and business fundamentals—with 3 hours of CLE-eligible content

Work with the right professionals:

- Financial advisors who specialize in legal professionals understand partner compensation, K-1 income, law school debt, and the income patterns unique to legal careers — nuances a generalist advisor is likely to miss

- The stakes are highest at the partnership transition or during a career change, when specialized guidance matters most

- Look for fee-only fiduciary advisors (NAPFA-listed) with documented experience serving attorneys

Build financial habits into your routine:

- Review monthly cash flow—even a 15-minute check is sufficient

- Track net worth quarterly; the trend matters as much as the number

- Schedule one formal financial planning session annually, or whenever a major career event is approaching

Consistency beats complexity. A simple system you actually use is worth far more than an elaborate one that sits untouched.

Frequently Asked Questions

What financial concepts should every lawyer know?

The essentials: net worth, cash flow management, tax efficiency (including business structure), debt repayment strategy, and the basics of retirement accounts—401(k), IRA, and SEP-IRA depending on your employment setting. Lawyers who understand these concepts early avoid the reactive financial decisions that derail otherwise successful careers.

What are the biggest financial mistakes lawyers make?

The most common: living up to income without building savings, delaying retirement contributions due to debt pressure, selecting the wrong loan repayment plan early, and failing to protect income with disability insurance.

How can lawyers manage law school debt while building wealth?

The right repayment structure is the starting point: IDR if you're PSLF-eligible, aggressive paydown or refinancing if you're heading to private practice. From there, automate retirement contributions in parallel—the amount matters less than the habit of starting.

Should lawyers work with a financial advisor who specializes in attorneys?

Yes. Attorneys have unique income structures, debt profiles, and tax situations—partnership buy-ins, K-1 distributions, phantom income, law school debt—that benefit from advisor familiarity with the legal profession rather than generalist advice.

How does financial literacy help lawyers who want to leave legal practice?

Knowing your financial baseline—savings, expenses, debt, and runway—converts an emotionally fraught decision into a concrete planning exercise. It shows what a transition actually requires, which is almost always more manageable than the fear suggests.

Is financial literacy relevant for salaried attorneys at large firms, or just solo practitioners?

Both. Salaried associates need to manage debt, build savings, and understand compensation structures. Partners and solo practitioners face additional complexity around taxes, equity, and business finances.